By Will Hubbard

The major U.S. stock indexes were up last week despite some volatility. The S&P 500 Index finished up 1.39%, the Dow Jones Industrial Average gained 1.18%, the NASDAQ Composite rose an impressive 1.66%, and the Russell 2000 small-capitalization index added 0.52%. The 10-year Treasury bond yield fell 5 basis points to 3.38%. Spot gold closed the week at $1,978.21, down 0.55%.

Stocks

As we approach the end of the first quarter of 2023, the economic and financial landscape has become difficult to navigate. Some of the data is awful. Inflation, interest rates, and problems in the banking sector are a quagmire. All of this is adding volatility to the equity markets.

And the government’s response to the banking crisis hasn’t helped. At the very least, it’s been confusing. For example, take recent events:

- Tuesday, March 21: Secretary Yellen’s prepared remarks to the American Bankers Association offered bank customers confidence that their deposits are safe: “Let me be clear: the government’s recent actions have demonstrated our resolute commitment to take the necessary steps to ensure that depositors’ savings and the banking system remain safe.”

- Wednesday, March 22: The Federal Open Market Committee (FOMC) announced a 0.25% increase to the federal funds rate, raising it to 5%. After the announcement, a reporter from the Economist asked Federal Reserve Chairman Powell about the safety of deposits. He replied, in part, that “depositors should assume that their deposits are safe.” This bolstered confidence in the regional banks with disastrous balance sheets following the rapid rise in interest rates over the last year. Investors and the market appreciate consistency, and consistency helps reduce volatility.

- On the same day as the FOMC release, Yellen testified before the Senate Appropriations Financial Services and General Government Subcommittee hearing and walked back her previous statement from the day before that all deposits are safe. In the subcommittee hearing, she said, “I have not considered or discussed anything having to do with blanket insurance or guarantees of deposits.”

- But two weeks ago, during a Senate Finance Committee hearing on the fallout of Silicon Valley Bank, Yellen explained what would need to happen for depositors of other institutions to be bailed out. In the event of a bank failure, you need a supermajority of the Federal Deposit Insurance Corp. (FDIC) and the Federal Reserve, as well as consultation from the Department of the Treasury, to bail out depositors.

On the economic data front, unemployment claims came in at 191,000 versus the anticipated 198,000. Figures for manufacturing and services PMI were also better than expected. The PMI composite rose at the fastest pace in over a year with new orders returning to growth mode. The PMI composite came in at 53.3, compared to 50.1 for February. This figure represents a 10-month high. Business confidence, however, remains weak. S&P Global reported that growth expectations for the next year were moderated due to inflationary pressures, financial market uncertainty, and higher interest rates.

Stocks, as represented by the S&P 500, were up overall. Yet the trading ranges for each day were more than 1%, representing the volatility around banking concerns in the short run and where future growth may come from in the months and years to come.

The best way to face uncertainty is to focus on tangibles, like data and historical context, and be prepared. Being prepared means considering all the tools and resources available to achieve your end goal.

Over the last decade or so, many U.S. investors have piled into domestic U.S. securities, embracing the home bias (investing in your own county at the expense of a robust and diversified portfolio). As a result, individuals and many professionals have shunned and underweighted international and emerging markets in their portfolios. As the dollar dips from its high and gold rallies toward all-time highs, investors should take another look at their portfolios.

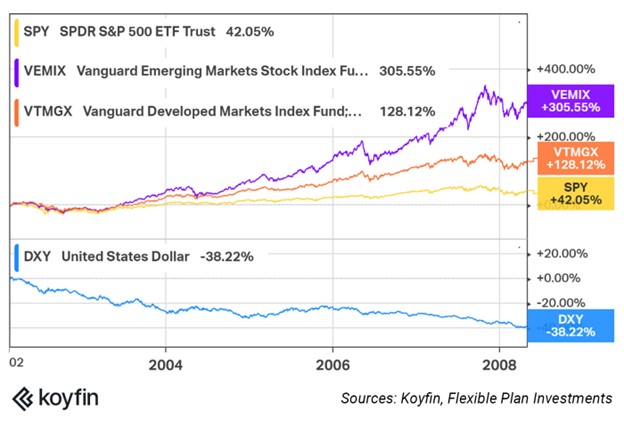

Since late 2020, the U.S. dollar has been incredibly strong, rising to heights not seen since the early 2000s. In October 2022, the dollar hit its current peak and has since retreated, offering a reprieve for assets that benefit from a weakening U.S. dollar. Going back to a previous secular dollar decline, when its value fell almost 40%, we see that emerging markets (represented by the Vanguard Emerging Markets Stock Index Fund, the purple line in the following chart) and international developed ex-U.S. markets (represented by the Vanguard Developed Markets Index Fund, the orange line) do well compared to developed U.S. (represented the SPDR S&P 500 ETF, the yellow line). Emerging markets outperformed by approximately 250%, and international developed markets outperformed by about 80%.

What this means for the future is that as interest rates shuffle and the global order we’ve known for the last decade gets shaken, considering non-U.S. investments and having a management style that can actively rotate with them could provide portfolio benefits.

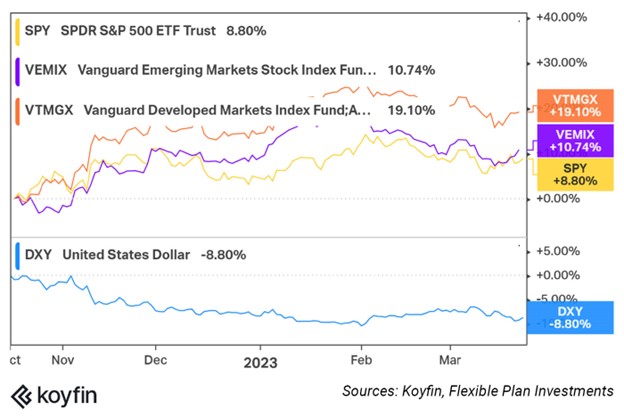

Looking at the period since October 15, we see a trend emerging. The S&P is up 8.8%, emerging markets are up 10.7%, international developed ex-U.S. markets are up 19%, and the U.S. dollar is down 8.8%. This tells us that non-U.S. and non-dollar-denominated investments become more attractive when the greenback loses its luster overseas.

There could be a point in the future when non-U.S. investing is in vogue again. Investors should look for risk managers that proactively search for and maintain methods to address these future challenges instead of scrambling to react after the fact.

Bonds

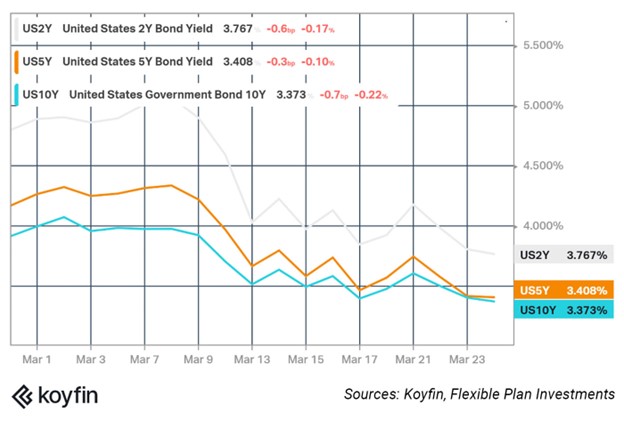

Bond yields had a volatile week. The two-year Treasury peaked near 4.2% heading into the FOMC announcement before falling to 3.76% on Friday (March 24), down from its high of roughly 5% earlier this month. The 10-year Treasury ended just above 3.38%, down from its earlier high of 4%.

Gold

Due to the FOMC meeting and Secretary Yellen’s conflicting comments concerning bank depositors, the yellow metal was volatile last week, down 2% by Tuesday (March 21) before rallying up almost a percent Thursday. On Friday, it closed about where it started, down 0.55%.

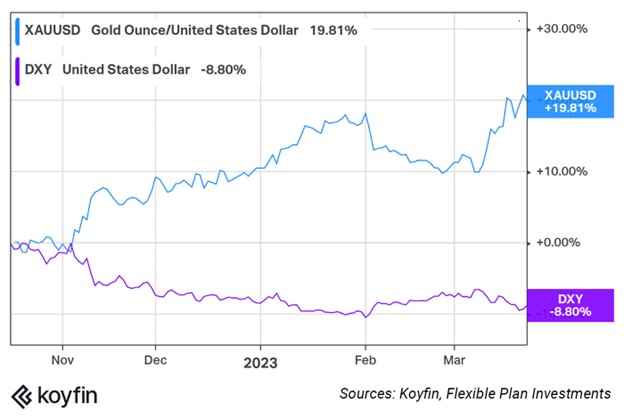

The theme for gold for quite some time has been its negative correlation to the U.S. dollar. That relationship hasn’t budged. Since mid-October 2022, gold has rallied nearly 20% while the dollar has slid almost 9%.

Flexible Plan Investments is the subadvisor to the only U.S. gold mutual fund, The Gold Bullion Strategy Fund (QGLDX), designed at its introduction nine years ago to track the daily price changes in the precious metal.

The Indicators

The very short-term-oriented QFC S&P Pattern Recognition strategy started last week 70% long. On Tuesday’s close (March 21), it moved to 50% short. By Wednesday, it was 110% short. On Thursday’s close, it reduced exposure again to 10% short. On Friday, it moved back to 50% short. Our QFC Political Seasonality Index started last week in its defensive mode and shifted into its 100% equity position on Wednesday. (Our QFC Political Seasonality Index is available—with all of the daily signals—post-login in our Weekly Performance Report section under the Domestic Tactical Equity category.)

Our intermediate-term tactical strategies have been varied in their degree of defensive positioning. The key advantages these strategies offer to investors are their ability to adapt to changing market environments, participate during uptrends, and adjust exposure to more defensive posturing during downtrends.

The Volatility Adjusted NASDAQ (VAN) strategy was invested in a money market fund all week. The Systematic Advantage (SA) strategy started last week 90% long and cut exposure to 30% long on Monday’s close. The strategy then edged up to 60% long on Tuesday’s close before cutting exposure at Friday’s close to 30%. Our QFC Self-adjusting Trend Following (QSTF) strategy was 100% long to start the week and increased exposure to 200% on Thursday’s close. VAN, SA, and QSTF can all employ leverage—hence the investment positions may at times be more than 100%.

Our Classic model was long risk-on positioning to start the week and moved into a defensive posture on Tuesday’s close. Most of our Classic accounts follow a signal that will allow the strategy to change exposure in as little as a week. A few accounts are on more restrictive platforms and can take up to one month to generate a new signal.

Flexible Plan’s Growth and Inflation measure, one of our Market Regime Indicators, shows markets are in a Normal economic environment stage (meaning inflation is rising and GDP is growing). This environment is the most common—accounting for 60% of the investable days since 2003—and favors stocks and gold. On average, gold has performed best during Normal market environments, but it comes with additional drawdown risk.

The S&P volatility regime is registering a High and Rising reading, which favors equities over gold and then bonds from an annualized return standpoint. The combination has occurred 23% of the time since 2000. It is a stage of relatively low returns and higher volatility for the three major asset classes.